US Health Insurance Terms: Premium, Deductible & More

Welcome to the wonderful world of health insurance, where the only thing more confusing than the plans is the price tag.

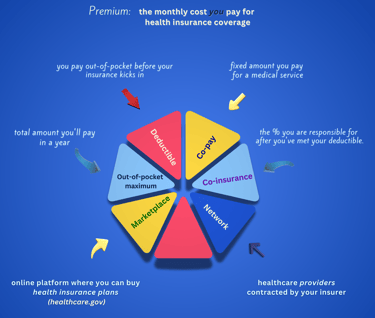

Let's start with Premium - because you gotta pay just to play!

Premium is your monthly subscription to the "Don’t Go Broke Club." It’s the amount you shell out every month, whether you use your insurance or not. Think of it like a gym membership—you pay for it, but whether you actually go (or in this case, get medical care) is another story.

🔹 Higher premium means lower out-of-pocket costs later (more like an all-you-can-eat buffet where you’ve already paid).

🔹 Lower premium means higher costs when you actually need care.

So, your premium is basically renting peace of mind that you won’t end up selling a kidney just to pay for a hospital visit.

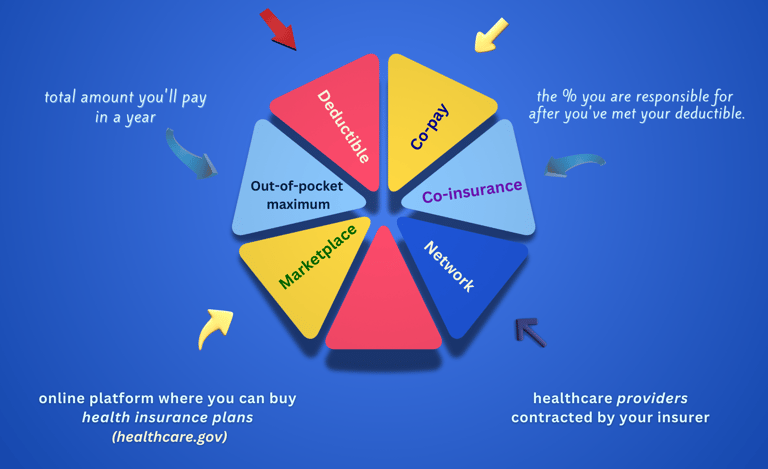

DEDUCTIBLE

Ah, the Deductible—insurance’s way of making sure you suffer just a little before they step in. Think of it like a cover charge at an exclusive club, except instead of VIP treatment, you get the privilege of finally using the benefits you already pay for.

Your deductible is the amount you have to pay out-of-pocket before your insurance even considers helping you out.

As a result, the higher your deductible, the lower monthly premium, but you’ll pay more when you need care. Great if you love living on the edge. Likewise, a low deductible plan means a higher monthly premium, but your insurance kicks in sooner.

Basically, the deductible is the insurance company’s way of saying, “Prove you really need help before we open our wallets.”

Now, about the weired 5 letters of CO-PAY

Just when you thought you were done paying, say hello to Co-Pay! This is the tiny (or not-so-tiny) fee you pay every time you visit a doctor in the US, get a prescription, or do anything remotely medical.

Think of it like a cover charge for healthcare—except the DJ is a doctor, and instead of drinks, you get a flu shot. Some plans have low co-pays (a few bucks per visit), while others make you fork over more.

On the brighter side, your co-pay is fixed, meaning you know what you’re paying each time.

CO-INSURANCE

So you met your deductible, but guess what? You’re not done yet. Co-insurance is the part where your insurance company still wants you to cover a percentage of the bill.

Example: If your plan says 80/20 co-insurance, your insurance pays 80%, and you’re still on the hook for 20% (because you agreed when you signed the plan).

Basically, co-insurance is insurance's way of saying, “We’ll help you, but only after you help yourself first".

OUT-OF-POCKET MAXIMUM (OOP Max)

Finally, a light at the end of the financial tunnel! Your Out-of-Pocket Maximum is the most you’ll ever pay in a year before your insurance covers 100% of everything (hallelujah!).

🔹 It’s like a “you’ve suffered enough” limit—after you hit this number, you stop paying for covered services. 🔹 But the Premiums don’t count toward this limit Only deductibles, co-pays, and co-insurance do.

This is why people with high medical expenses might choose a plan with a lower OOP Max—it limits the total financial hit.

Next up: Network - because not all doctors are on your insurance company’s VIP list.

NETWORK

Think of Network as your insurance company’s VIP list. These are the doctors and hospitals they actually like—which means if you see them, you’ll pay less.

In-Network: These are the healthcare providers your insurance is BFFs with (thus, lower costs for you!). Out-of-Network: The ones your insurance doesn’t like, meaning you’ll pay way more to see them.

We would strongly recommend to check the network before scheduling an appointment unless you enjoy financial surprises.

MARKETPLACE

The Marketplace is basically the Amazon of health insurance. It’s an online platform (like healthcare.gov) where you can compare and buy different health plans.

If you don’t get insurance from work, this is where you go to shop for one. Plans come in different flavors—Bronze, Silver, Gold, and Platinum (no, it’s not a rewards program, just different cost levels).

Think of it like picking a cell phone plan - except instead of unlimited data, you’re choosing how much pain your wallet can handle when you go to the doctor.

At the end of the day, health insurance is like a confusing game where you pay upfront, follow a bunch of weird rules, and still get hit with surprise fees. But love it or hate it, having coverage is the difference between a manageable bill and financial ruin.